As of late February 2026, total U.S. national debt has surpassed $38.7 trillion. At the end of 2025, American household debt reached a record $18.8 trillion, including mortgages, auto loans, student loans, and credit cards. The average total consumer debt per household is approximately $105,056, with credit card debt, alone, hitting a record $1.28 trillion.

Those are big numbers. The kind that makes you want to sit down—even if you’re already sitting down.

An old friend once joked that he was a proud American because he was in debt up to his eyeballs.

That national backdrop may help explain why I’ve heard so many questions lately about our projects, cost overruns, and whether Heritage Palms itself is in debt. It comes with the territory in a community like ours – where many residents are careful with their spending, think twice about carrying a credit card balance, and still manage to tip the staff generously. We may debate pickleball line calls, but we take financial stewardship seriously.

As Adam Smith once said, “What can be added to the happiness of a man who is in health, out of debt, and has a clear conscience?” Around here, we might add: and holding a decent tee time.

So, let’s talk about projects and debt. The key question is simple: “Is Heritage Palms in debt?” To answer that, we need to look at what has happened over the past several years.

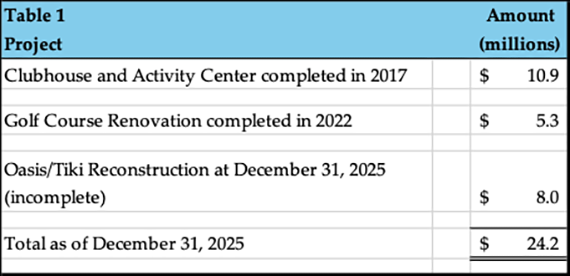

Over the last decade, the Club has made significant facility improvements. The Clubhouse was renovated, a new Activity Center was opened, the golf courses were updated, and the Oasis/Tiki project was recently completed. None of that happens with spare change found in the sofa cushions. It takes real money, and the following table shows how much was required.

Please note that the final cost of the Oasis/Tiki project will not be known at the time of publication. (Yes, I know – that sentence makes accountants and engineers equally nervous.)

These investments have more than doubled the Club’s total assets since 2017. That represents a substantial commitment – and a valuable upgrade to our community. We didn’t just repaint a few walls; we meaningfully enhanced the place we call home.

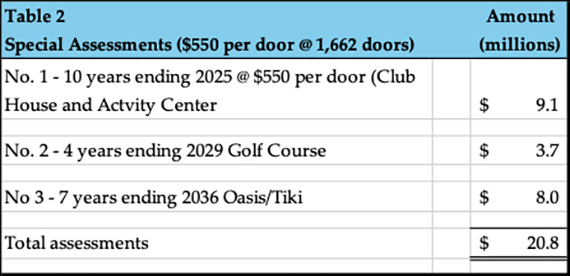

So how are we paying for these new amenities? As everyone knows, the membership approved three separate special assessments, as shown below. In other words, this wasn’t done quietly in the back office. The membership voted, and the membership is funding it.

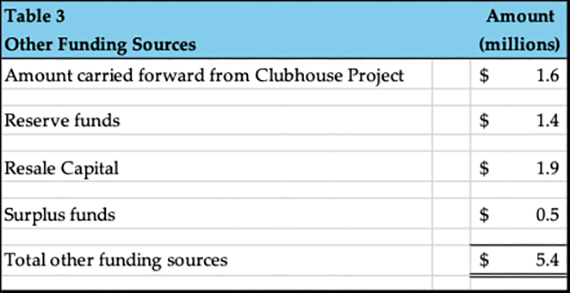

If total project costs are $24.2 million and the special assessments generate $20.8 million, doesn’t that leave a shortfall? Yes, it does. However, the Club has additional sources of cash to bridge the gap. Those sources are outlined below. (No bake sales required.)

One important point about Table 3: it reflects available sources as of December 31, 2025. The Club will continue to receive resale capital contributions in 2026 and in future years. In addition, it is likely that some operating surplus funds will be allocated to the projects. This is especially relevant because the final Oasis/Tiki cost has not yet been determined and may exceed initial estimates. Construction projects and original budgets are not always close friends.

The bottom line is this: The membership is funding these projects at the level required. Combined with other available sources, those funds are sufficient to pay for these new amenities. Now, back to the question of debt.

Note 8 to the Audited Financial Statements for the year ended December 31, 2025 (available on our HP website), discloses that the Club has a $10 million loan commitment from a bank. This is more appropriately known as a “Line of Credit” which is like a Home Equity Line of Credit. It’s secured by the Club’s special assessments and its initiation, transfer, and estoppel fees. The interest rate is the Secured Overnight Financing Rate (SOFR) plus 1.9%, which currently equates to approximately 5.6% to 5.7%. Not giveaway money – but also not payday-loan territory.

This financing arrangement was put in place to manage cash flow. So far, the Club draws on the Line of Credit during the late summer and fall and repays those draws during December as Master Dues and Assessments arrive in the bank account. As of December 31, 2026, there is no balance on the Line of Credit. In other words, the line of credit is there if needed – but it’s not being used as a lifestyle choice.

So, what does all this mean?

In my judgment, it means the Club has a thoughtful and disciplined financing plan for these important projects. We are each paying our share annually – as we should – but we were not asked to write a single $15,000 check upfront. I suspect that would have caused more heartburn than Taco Tuesday.

Instead, the costs are being managed prudently, spread over time, and supported by a financing structure at a reasonable interest rate. The line of credit is there as a cash- flow tool – not as a sign that we’re living beyond our means.

In other words, Heritage Palms is not “in debt up to its eyeballs.” We have invested in our community, planned carefully for how to pay for it, and positioned ourselves to enjoy the improvements without financial drama.

That’s not flashy. It’s not exciting. But from a number’s standpoint – and for those of us who sleep better knowing the bills are covered – that’s exactly how it should be.